If you sit anywhere near product, engineering, or ops right now, you’ve probably had some version of the same conversation this year: are we actually doing anything with “agentic AI,” or are we just nodding at conference talks? A year ago it was a curiosity people dropped into Slack threads; now it’s creeping into OKRs and budget reviews.

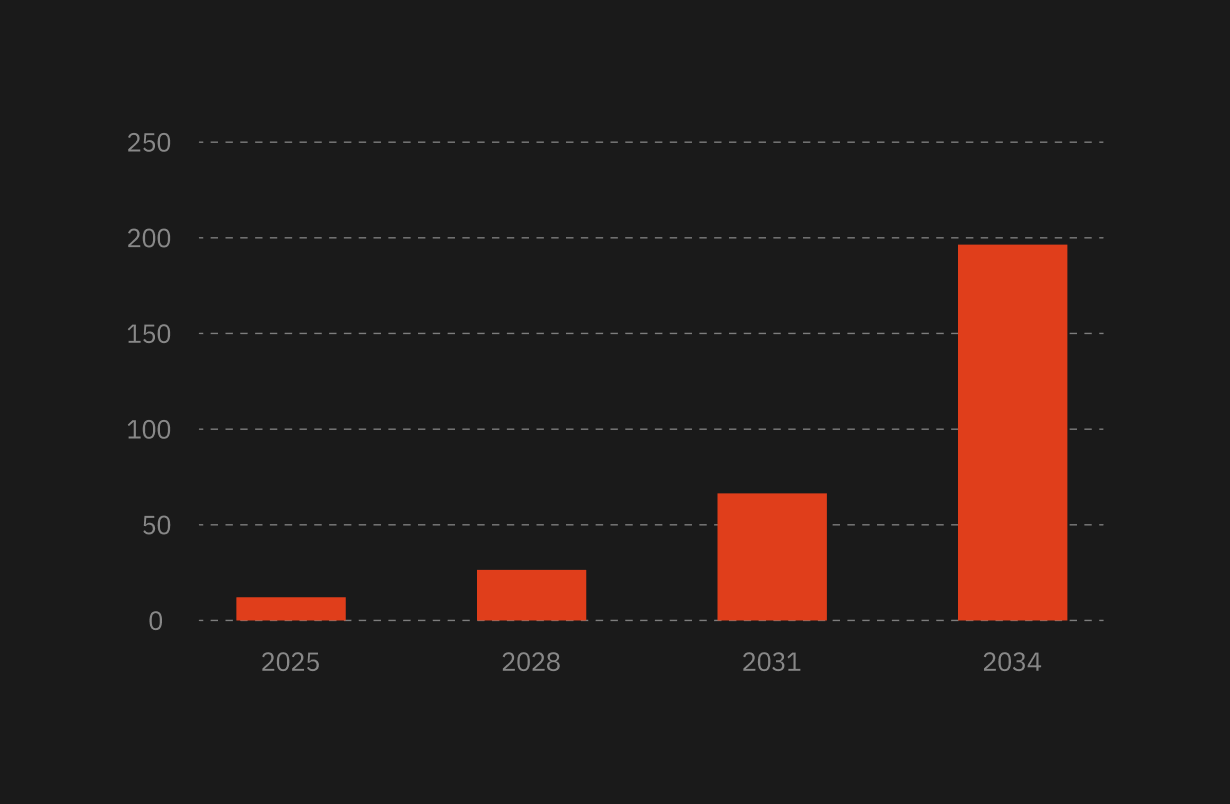

The market numbers are starting to catch up to that shift. Depending on which report you read, 2025 revenue for agentic AI lands somewhere around $7.3–8.8 billion. Push those curves out to 2034 and the estimates jump into roughly the $139–324 billion range, which works out to something like 40–44% growth per year. Nobody knows the exact landing spot, but the direction is pretty clear.

%20(1).png)

Inside companies, surveys paint a similar picture. Across a bunch of them, you see about three-quarters of organizations saying they’re either already using agents or actively testing them. And if the current forecasts hold, by mid-2026 roughly 40% of enterprise applications will ship with some kind of agent baked in.

That’s the backdrop. The interesting part is less “how big is the market” and more “who’s actually paying for this, where is it working today, what payback teams are seeing, and why so many pilots never quite make it into the systems that run every single day.”

Follow the money: VC and enterprise budgets

By 2026, the question isn’t “is there money here?” anymore. It’s “who’s writing the cheques, and for what?”

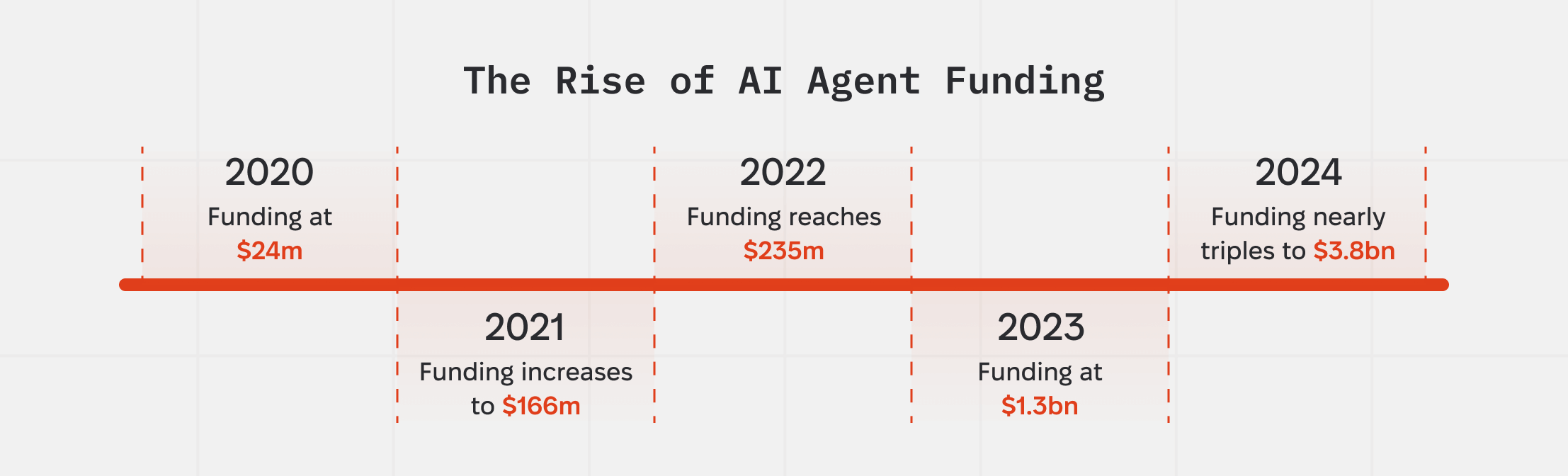

On the VC side, the slope over the last few years is pretty clear. In 2023, agentic AI startups raised a bit over $1.3B. In 2024 that was closer to $3.8B. By the first half of 2025 they’d already taken in roughly $2.8B; if you crudely annualize that, you end up somewhere around $6.5–7B for the year — roughly three-quarters more than 2024.

A few deals put some names to those curves:

- Salesforce Ventures set up a $500M AI fund and has deployed about $1B into AI startups over roughly 18 months;

- Anysphere (Cursor) raised around $900M at a $9B valuation;

- Hippocratic AI in healthcare moved past the $500M valuation mark.

These aren’t “let’s see what happens” seed bets.

If you look at AI more broadly, the backdrop is even bigger. In 2024, total AI venture funding across categories pushed past $100B, up something like 80% year on year, and agentic companies are steadily taking a larger slice of that.

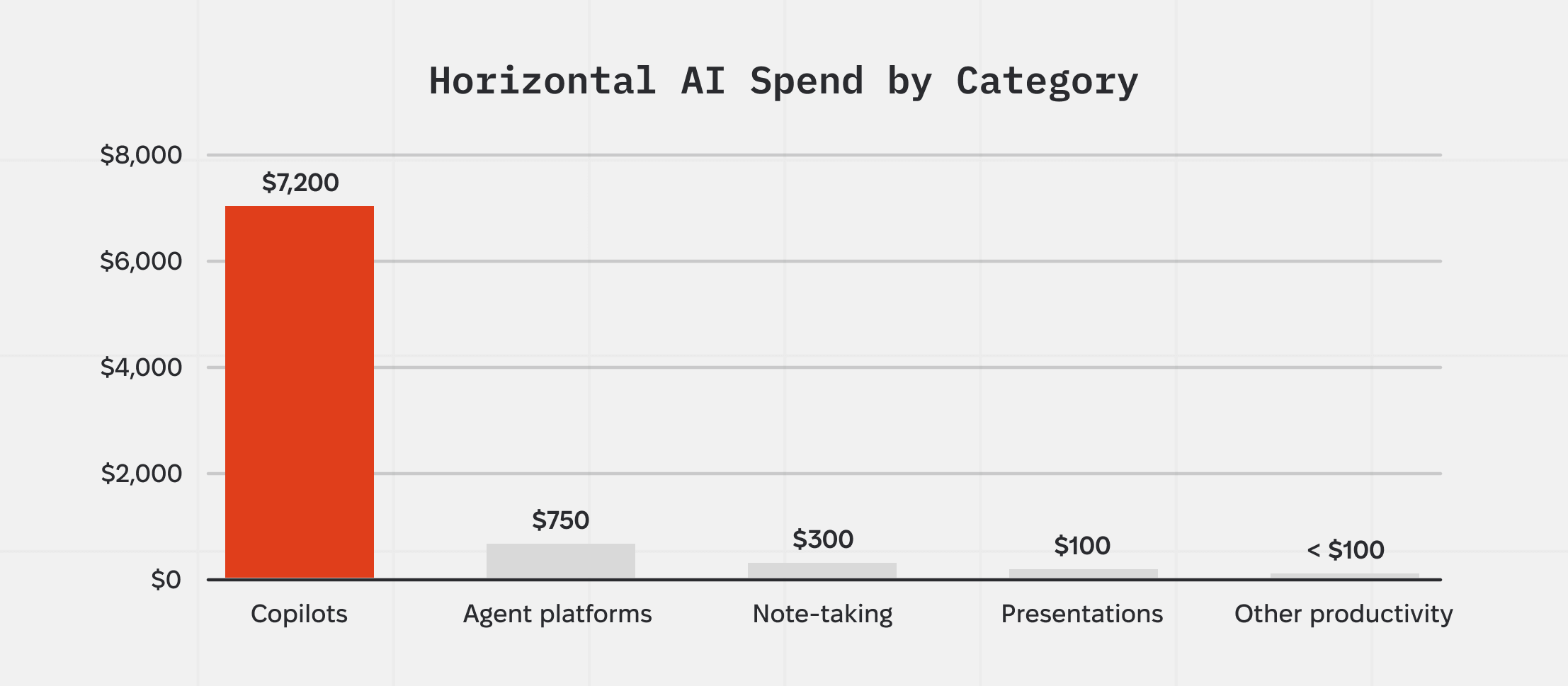

Enterprise budgets have followed the same direction. By the end of 2025, organisations were spending around $37B on AI — roughly three-plus times 2024 and about 6% of global SaaS spend. Roughly half of that, about $19B, went straight into applications, more than half of all generative AI spending. Meanwhile, horizontal AI is still the big one in the application layer: about $8.4B in revenue, up roughly 5.3x year over year. Most of that is copilots, which hold around 86% of the category (about $7.2B). Another 10% (roughly $750M) sits with agent platforms and the remaining 5% (about $450M) goes to personal productivity tools.

The build-vs-buy instinct has flipped too. Instead of a near 50/50 split, roughly three-quarters of AI use cases now run on vendor products, not internal projects.

Surveys going into 2026 are pretty blunt about what happens next: somewhere in the mid-80s percent of leaders say they expect to increase spending on AI agents over the next year, and close to nine in ten senior execs say their teams are growing AI budgets specifically because agents are starting to deliver real value.

If you’re shipping software in 2026, that’s the environment you’re walking into. Buyers already have a line item for agents and a short list of workflows they’re hoping you’ll take off their plate.

Adoption: what’s really live vs. “in pilot”

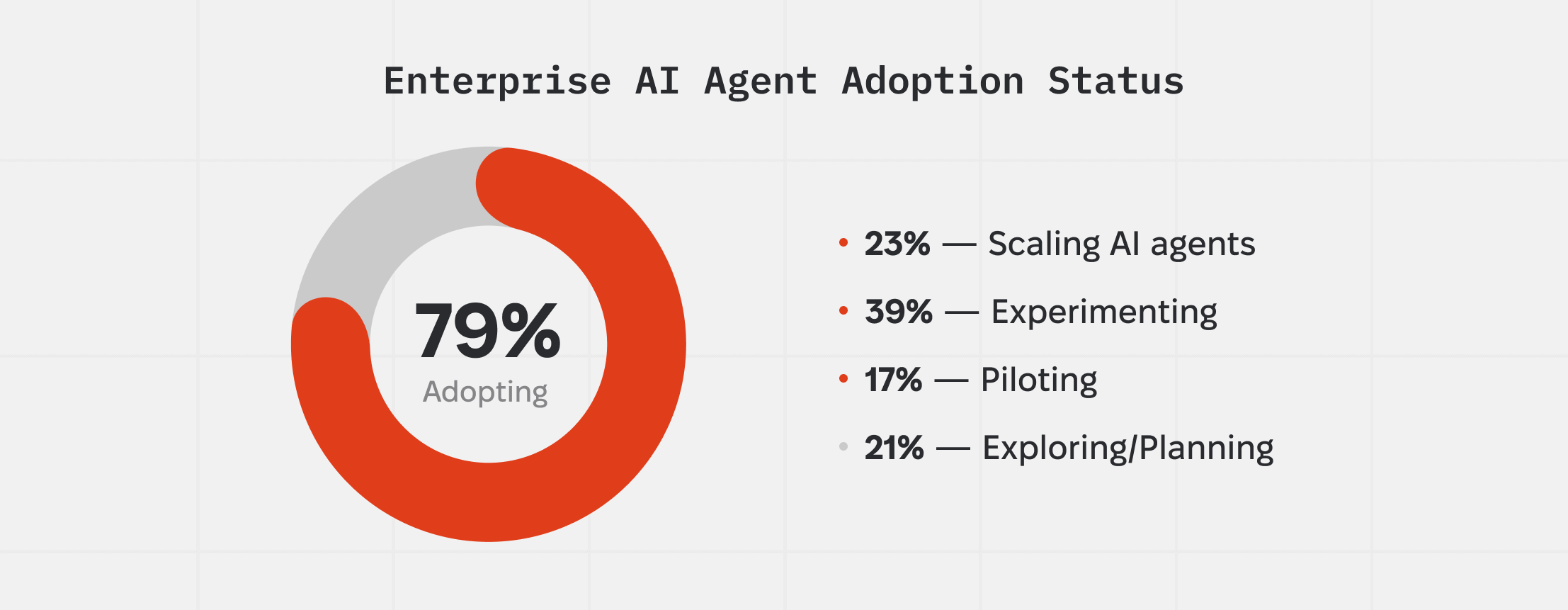

On paper, adoption looks huge: 72–79% of enterprises say they’re either deploying or actively testing agentic systems.

The more interesting view is maturity. Split out, it looks roughly like this:

- 23% say they’re scaling agents across production workflows

- 39% are experimenting (POCs, internal labs, evaluations)

- 17% are in pilot

- 21% are still planning or haven’t really started yet

So yes, most organizations have a slide about agents. Only about a quarter are at the stage where autonomous workflows are part of the normal day.

And then there’s application penetration. In 2024, fewer than 1% of enterprise applications had agentic capabilities. Analysts expect that to jump to something like 40% by mid-2026, and around 33% by 2028.

So we’re in an odd transition period:

- At the organization level, agent initiatives are everywhere.

- At the application level, most tools are still pre-agent, but the slope over the next 24–36 months is very steep.

Add in one more uncomfortable number: only about 11% of pilots actually make it into full production. The model demos fine, the slides look good, and then the rollout runs into integration, governance, and change-management friction.

Do the returns justify the effort?

If you ask, “Is this actually paying for itself, or are we just entertaining ourselves with new toys?”, the data so far leans toward yes, it pays.

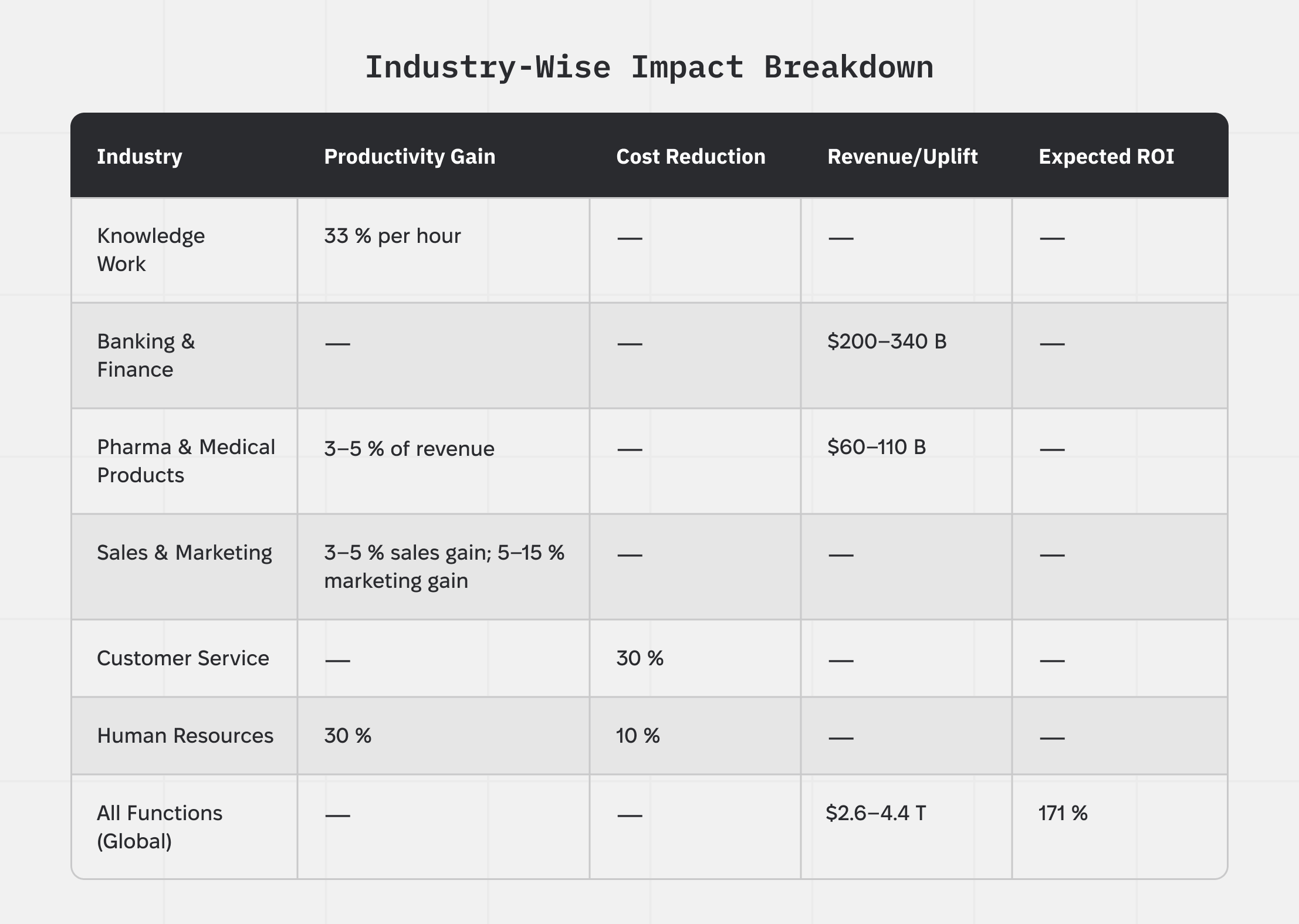

In the survey work behind this piece, about 62% of organisations using agents say they expect returns above 100% on their investments, and the average expectation lands around 171%.

When people report on projects that are already finished rather than planned, the picture is similar: across large programmes, we see a median return of roughly $175M, an average around $221M, against about $187M in implementation spend. These are self-reported numbers, so you should mentally shave a bit off for optimism and survivor bias, but even after that haircut they’re hard to dismiss.

The smaller, everyday effects line up with that story. Roughly 80% of organisations that have agents in production say they can point to clear gains. At the individual level, people are getting back somewhere in the 40–60 minutes per day range once agents pick up the repetitive work—copying between systems, basic follow-ups, status checks. Teams that live on repeatable workflows talk about 25–35% efficiency bumps, and customer-facing groups tend to sit at the high end, because trimming a minute off hundreds of interactions a week quietly moves real numbers.

By 2026, that’s usually enough for finance and leadership: the conversation inside most companies isn’t “does this make money?” anymore, it’s “where do we point it next, and how careful do we need to be when we plug it into the rest of our stack?”

Where agents are actually showing up

If you look past the hype and focus on real deployments, four areas keep coming up first: support, healthcare, security/ops, and finance/risk. That’s where “autonomy + tools” is already changing the cost curve, not just the demo reel.

Customer support and contact centers

Most teams start with support because it’s the cleanest fit: high volume, repetitive patterns, and clear success metrics.

Cisco’s 2025 survey expects a bit more than half of all support interactions to involve agentic AI by mid-2026, and roughly two-thirds by 2028. That’s not just theory. In mature setups, agents comfortably handle the bulk of routine tickets, and humans spend their time on the odd cases instead of password resets all day.

Across vendors, the numbers look surprisingly similar: agents own somewhere near 80% of simple queries end-to-end, first response times drop by around 50%, and for the flows that are properly designed you see resolution rates in the high-90s. Ada, for example, talks about automated resolution in the low-80s percent range and ROI that can hit double-digit multiples.

You can see the same pattern in public reference cases:

- Shopify has talked about roughly halving the workload on human agents after rolling out AI.

- Airbnb reports response times roughly 30% faster.

- Bank of America’s Erica now deals with about 1.5M customer requests per day.

Once you’re at that scale, you’re not “saving a few minutes per ticket” anymore; you’re running a support org whose first line is an agent layer, with humans supervising rather than carrying every interaction themselves.

Healthcare and life sciences

Healthcare looks very different and, if anything, is growing faster than the rest of the agentic space.

Market estimates put AI in healthcare around $21.66B in 2025, with projections jumping to roughly $110.61B by 2030 — about 48% compound growth, faster than the broader market. Regulators are clearly not blocking everything: in just the first half of 2025, 127 AI medical devices were approved.

On the clinical side, systems in places like Mayo Clinic report close to 89% diagnostic accuracy on complex cases and about a 60% reduction in diagnostic time when agents help with triage and suggestion. On the “paperwork” side, agents shorten intake and documentation, handle insurance checks, and move data through billing.

Revenue cycle management is where this hits the balance sheet. At Easterseals Central Illinois, agentic RCM tools helped cut accounts receivable by 35 days and reduce primary claim denials by 7%. For a provider, that’s the difference between constantly chasing cash and having a bit more breathing room.

Cybersecurity and IT operations

Security and IT ops teams were always going to try this early. Their world is logs, alerts, and playbooks — exactly the kind of environment where an agent can sit and grind all day.

PwC’s data suggests that around 53% of US businesses using agentic AI point it at IT and cybersecurity: threat detection, incident triage, vulnerability management, plus the usual run-ops work. In telecom, adoption is even more aggressive: roughly 97% of specialists say they’re adopting or at least assessing AI in operations, and about half are already using it.

When it works, this doesn’t turn into “the AI runs the SOC on its own.” It looks more like a team of tireless junior analysts: agents pull context from different tools, correlate signals, propose responses, and automatically take the low-risk actions (close obvious false positives, gather more evidence), while humans drive the calls that actually matter.

Finance and risk

Finance and risk teams use agents with a slightly different agenda: less “wow factor,” more “make sure money and obligations are where they should be.”

Typical jobs here:

- watching transactions in real time for anomalies

- stopping fraud before execution instead of just flagging it afterwards

- taking over repetitive pieces of AML / KYC workflows

- assembling and checking regulatory reports so humans are reviewing rather than building from scratch

Technically, most of this is straightforward with today’s tools. The harder part is governance: who can approve a blocked transaction, which systems an agent is allowed to touch, how you log and explain a decision when a regulator shows up six months later.

Key market barriers and implementation challenges

By 2026, “we’ve got a couple of agent pilots running” is a pretty standard sentence. The interesting part is what people say right after that — usually some version of “but…” The same three problems keep turning up in that second half of the sentence: the state of the systems, fear of risk, and the fact that not enough people really know how to work with this stuff yet.

On the systems side, integration hurts the most. In the surveys behind this piece, around six in ten leaders put legacy and fragmented architecture at the top of their list.

.png)

You see why when you look under the hood: a CRM from one era, a core system from another, half a dozen internal tools, and a bunch of spreadsheets quietly holding the business together. None of that was designed for an autonomous process to read from and write back to. So the “agent” work very quickly turns into “fix the data model, build sane APIs, and unearth that one integration nobody has touched in eight years.” Financial services is the most obvious version of this. Banks have glossy digital fronts, but agents still have to talk to old core systems that disagree with each other about basic facts like balances or customer status. The model isn’t the bottleneck; the plumbing is.

Then there’s the risk conversation. Roughly 60% of respondents in enterprise surveys list some combination of risk, compliance, or governance as a major barrier, and the concerns are pretty reasonable. People don’t yet fully trust autonomous decisions, especially where money, permissions, or customer communication are involved. Giving an agent tool access also creates new ways for things to go wrong — misconfigurations, prompt-level attacks, or just badly scoped permissions. On top of that, the rules are still moving. The EU AI Act, the NIST work on AI risk, and tougher SEC expectations are all coming into force over the next few years. IDC even projects that by 2030, up to one in five G1000 organisations could end up with lawsuits, fines, or leadership changes tied to poor AI agent governance. You don’t have to believe the exact number to understand why security, legal, and risk teams now insist on basics like: being able to see what the agent did, having an audit trail for important actions, and putting a policy layer between agents and critical systems.

Even if you get those two sorted, you still run into the skills gap. Across studies, roughly a third of employees say ongoing AI training is the hardest part of adoption. The split by seniority is telling: about 41% of entry-level staff feel under-equipped to use AI features day to day, compared with roughly 10% of executives who say the same. Leadership is excited; the people in the tools all day are trying to keep up. At the company level, around three-quarters of organisations admit they don’t yet have the internal expertise to really scale generative AI. That’s where you see pilots that never quite grow up, “prompt wizards” who become a single point of failure, and multi-agent systems being treated like slightly fancier chatbots instead of workflows that need design, ownership, and runbooks.

Put together, those three things — messy foundations, fear of letting something autonomous touch real systems, and a thin bench of people who know how to do this properly — explain a lot of the gap between “we’ve got a demo” and “this agent quietly runs in the middle of our production stack every day.”

Conclusion

The real question for 2026 is simple: can we treat agents like production software, not like clever features?

If we can’t answer these plainly, we’re still in demo-land:

- What is the agent allowed to do, exactly? (permissions, tool allowlist, spend/time/retry budgets)

- How does it prove it did it? (receipts, confirmations, post-action reads, audit trail)

- What happens when it’s wrong? (escalation paths, safe stops, compensation, “who owns the failure”)

- How do we ship changes without roulette? (versioning, evals, canaries, rollback, runbooks)

- How do we measure it like a system? (SLOs for latency/accuracy, containment rate, cost per completed task)

That’s the bar. Agentic AI becomes “core infrastructure” only when it’s bounded, observable, and owned. Everything else is a chatbot with delusions of grandeur.